As the cash market open approached, it became apparent that volume had shifted from the ES September contract to the ES December contract overnight, so I made the switch. The offset was about 6.5 points, so I had to adjust today’s DTG levels by subtracting 6.5 from the published levels to work with the December contract. The price patterns and opportunities are generally the same between contracts, but I prefer to watch where most of the institutions are trading and starting today, that was the December contract. Contract rollover is always a difficult time if using volume as part of your decision making since volume gets divided between two contracts. On Monday, we’ll be completely moved over to the December contract and that will be reflected on the published DTG levels.

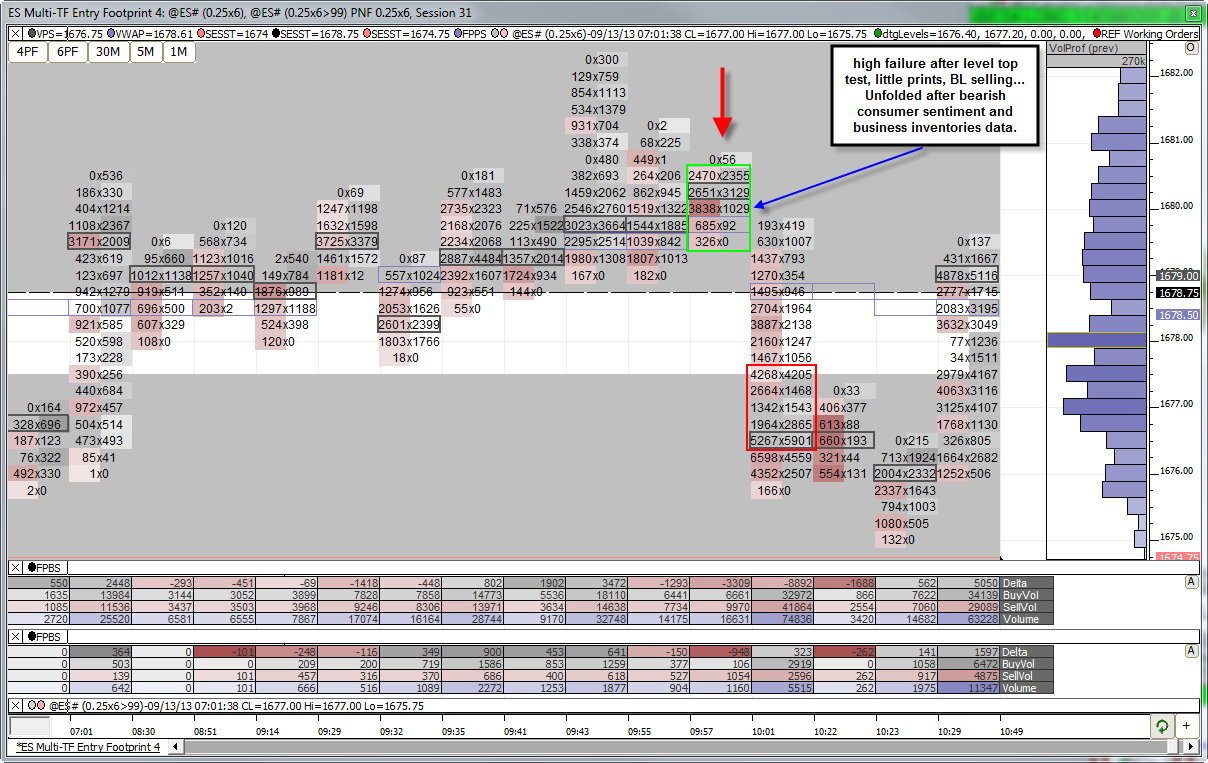

The markets reacted little to this morning’s disappointing Retail Sales number and positive PPI. Thus the ES came into the cash market hovering around it’s yesterday’s close without much incentive to move until traders could evaluate the Consumer Sentiment and Business Inventories numbers. Both came in bearish. After an initial postive reaction to the sentiment number, the ES bounced off the R1 pivot near the top of the adjusted DTG 78.75 level. Then business inventories also missed and a short order flow opportunity unfolded for today’s example trade.

| Below is member only content. Not a member? Subscribe and join the discussion!. Click here to become a member |

Sorry, the comment form is closed at this time.